Mutual funds in India

The first introduction of a mutual fund in India occurred in 1963, when the Government of India launched the Unit Trust of India (UTI). Mutual funds are broadly categorised into three segments: equity funds, hybrid funds, and debt funds.

- The total Assets Under Management (AUM) of the Indian mutual fund industry stood at ₹50.78 trillion (US$600 billion) in December 2023.

- According to SEBC, during FY 2022-23, 73% of mutual fund units were redeemed within 2 years of investment. Only investments in 3% of the units continued for more than 5 years.

- According to the Reserve Bank of India report, mutual funds attracted 6% of household savings in FY2023 and less than 1% went into direct equities. [5][6][7] Almost 95% of household savings in India park their money in bank deposits, including fixed deposit, provident fund, PPF, life insurance, and various small savings schemes. [5][6][7]

- According to the Reserve Bank of India report, mutual funds attracted 6% of household savings in FY2023 and less than 1% went into direct equities.[5][6][7] Almost 95% of household savings in India park their money in bank deposits, including fixed deposit, provident fund, PPF, life insurance, and various small savings schemes.

- According to the S&P SPIVA Report FY2022, over a 10-year period, approximate 68% of the large-cap actively managed funds failed to beat their respective benchmarks, and over 50% failed to beat their benchmarks in the mid- and small-cap segments.[8] Within the ELSS funds category, over 60% failed to beat their respective benchmarks over 10 year period.[8] Globally, over long periods of time, passively managed funds consistently outperform actively managed funds

Mutual fund statistics

| Holding Period | Units redeemed in FY22 ▲▼ | Units redeemed in FY23 ▲▼ |

|---|---|---|

| 0 - 1 years | 56.83% | 50.11% |

| 1 - 2 years | 15.14% | 23.04% |

| 2 - 3 years | 5.03% | 9.81% |

| 3 - 5 years | 20.41% | 13.96% |

| More than 5 years | 2.59% | 3.09% |

- AUM of Equity funds - ₹20.33 lakh crore (US$240 billion) (November 2023)

- AUM of Hybrid funds - ₹6.90 lakh crore (US$82 billion) (January 2024)

- AUM of Debt funds - ₹11.97 trillion (US$140 billion) (March 2020)

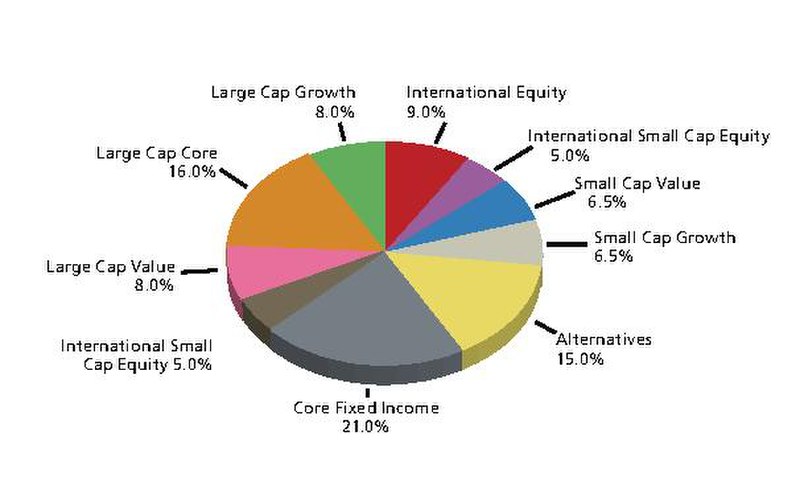

Mutual fund category breakup

Controversies

List of Mutual fund companies/schemes bankrupted, defaulted or closed

2020 Franklin Templeton Mutual Fund fiasco

In April 2020, Franklin Templeton India unexpectedly wound up six credit funds with assets of close to $4 billion, citing a lack of liquidity amid the coronavirus pandemic. These funds had large exposure to higher-yielding, lower-rated credit securities. The Securities and Exchange Board of India (SEBI) conducted a probe into this sudden closure and found “serious lapses and violations”. As a result, in June 2021, SEBI barred Franklin Templeton Mutual Fund from launching any new debt schemes for two years. The regulator also ordered the fund house to refund investment and advisory fees, along with interest, of more than 5 billion rupees, and fined the global giant another 50 million rupees. [15][16][17][18]

Franklin Templeton said it strongly disagreed with the SEBI’s order and planned to appeal against it. The decision to wind up the schemes “was taken with the sole objective of preserving value for unitholders”, a spokesperson said. However, the closure of these funds sparked panic withdrawals from other Franklin Templeton schemes as well as credit funds of other asset managers, leading to a storm on social media and court cases by distraught investors.

Reliance Mutual Fund

In 2019, the debt schemes of Reliance Mutual Fund faced a liquidity crisis due to their exposure to troubled companies like Dewan Housing Finance Corporation (DHFL). This led to severe redemptions and forced asset sales, which significantly affected investors.

IL&FS crisis and impact

The IL&FS crisis in 2018 had a significant impact on the mutual fund industry, including those managed by IDBI Mutual Fund. The defaults by IL&FS led to a series of downgrades and defaults on its debt obligations and inter-corporate deposits1. This situation caused considerable distress in the financial markets and led to significant markdowns in the Net Asset Values (NAVs) of the affected mutual fund schemes, resulting in losses to investors.

Investor confidence in debt mutual funds, particularly those with high exposure to NBFCs and infrastructure debt, was severely undermined. This led to significant outflows as investors moved towards safer and more liquid investment options. In response, the Securities and Exchange Board of India (SEBI) introduced stricter regulations on sectoral exposure, single issuer limits, and the quality of collateral accepted in debt funds to enhance liquidity and reduce risks. Fund managers began focusing on higher-quality assets and improved risk management practices. The crisis underscored the need for better credit assessment and liquidity management, prompting regulatory reforms and a more cautious investment approach within the mutual fund industry

Amtek Auto Impact

Several mutual funds, including those managed by JP Morgan Asset Management India, faced significant issues due to exposure to Amtek Auto, which defaulted on its debt in 2015. JP Morgan had to suspend redemptions and impose exit loads to manage the liquidity crisis

Birla Sun Life Mutual Fund (Aditya Birla Sun Life Mutual Fund)

In 2018, Aditya Birla Sun Life Mutual Fund faced redemption pressures in some of its debt schemes due to exposure to entities like the Essel Group companies. The Economic Times reported that the Aditya Birla Sun Life Mutual Fund was the biggest investor in the Essel Group, with an exposure of Rs 2,936 crore spread across 28 schemes1. This accounted for almost 37% of the total debt fund exposure to the Zee group, which is part of the Essel Group.

Dewan Housing Finance Corporation (DHFL) crisis and impact

The Dewan Housing Finance Corporation (DHFL) crisis had a profound impact on the Indian mutual fund industry. DHFL's defaults created a severe liquidity crunch, making it difficult for mutual funds to meet redemption pressures without selling assets at heavily discounted prices. This crisis raised significant concerns about the creditworthiness of housing finance companies (HFCs) and non-banking financial companies (NBFCs), leading to downgrades of DHFL's debt instruments and adversely affecting the net asset values (NAVs) of mutual funds holding these securities.

Investor confidence in debt mutual funds, especially those with high exposure to HFCs and NBFCs, was severely shaken, resulting in substantial outflows as investors sought safer investments. In response, the Securities and Exchange Board of India (SEBI) increased scrutiny and introduced tighter regulations on mutual funds' exposure to individual issuers and sectors to mitigate such risks in the future. Fund managers adjusted their portfolios by shifting towards higher-quality and more liquid assets, reducing exposure to high-risk debt instruments. The crisis underscored the importance of credit quality and liquidity management, prompting regulatory reforms and a more cautious approach within the mutual fund industry

2001 UTI Mutual Fund (Unit Trust of India) fiasco

The Unit Trust of India (UTI) faced a significant crisis in 2001, which was primarily due to large-scale redemption pressures and mismanagement, particularly in its flagship scheme, US-6412. The crisis was exacerbated by the Ketan Parekh scam, which caused a sharp decline in stock prices, leading to mutual funds, including UTI’s schemes, suffering severe consequences.

The government intervened to protect investors and restructured UTI. This restructuring led to the bifurcation of UTI into two separate entities in 2003: the UTI Mutual Fund (now managed by the UTI Trustee Company Pvt. Ltd.) and the Specified Undertaking of the Unit Trust of India (SUUTI), which took over the assets and liabilities of the erstwhile UTI12. The government’s intervention included a bailout package to stabilize the situation and ensure the protection of investors’ interests.

DHFL Pramerica Mutual Fund

Dewan Housing Finance Corporation Limited (DHFL) defaulted on its debt obligations in 2019. This event led to significant governance concerns and defaults by DHFL in meeting various payment obligations, prompting the Reserve Bank of India to supersede the Board of Directors of DHFL1. The default affected several mutual funds, including those managed by BNP Paribas Asset Management India Private Limited, which had to mark down the value of their investments in DHFL’s securities.

The crisis deepened with rating downgrades and write-offs by mutual funds, which had a cumulative exposure of ₹5,336 crore to securities issued by DHFL3. As a result, there was a severe liquidity issue and a drop in the Net Asset Values (NAVs) of the mutual funds, impacting investors’ returns. DHFL Pramerica Mutual Fund, which was a joint venture between DHFL and Pramerica Financial, Inc., also faced challenges due to the exposure to DHFL’s debt instruments

Yes Mutual Fund

In 2019, Yes Bank faced severe financial stress and was eventually placed under a moratorium by the Reserve Bank of India (RBI) in March 2020. This led to significant challenges for Yes Mutual Fund, particularly its debt schemes that had exposure to Yes Bank’s securities. The crisis necessitated write-downs and affected investor confidence. Around 32 mutual fund schemes had exposure to Yes Bank’s downgraded debt papers, with a total exposure amounting to approximately ₹2,848 crore. The crisis led to write-downs of these securities and impacted the net asset values (NAVs) of the mutual funds involved, which in turn affected investor confidence.

Kotak Mutual Fund

HDFC Mutual Fund did face a situation in 2018-2019 due to its exposure to companies like Essel Group and IL&FS. The credit events involving these companies led to significant mark-downs in the Net Asset Values (NAVs) of some of HDFC Mutual Fund’s debt schemes. This situation resulted in investor concerns and redemption pressures.

To elaborate, the IL&FS crisis was one of the biggest financial crises in India, with the company defaulting on several of its obligations due to a cash shortfall. The debt involved was about Rs 1 lakh crore. Similarly, Essel Group companies were grappling with debt woes, which put mutual funds, including HDFC, under redemption pressure. However, HDFC Mutual Fund later recovered the entire investment made in the non-convertible debentures issued by Essel Group companies.

Sahara Mutual Fund

SEBI conducted an examination to determine whether Sahara Mutual Fund, its Asset Management Company, and its trustees were ‘fit and proper’ as per regulatory standards. This was in light of a previous SEBI order from 2011 concerning two other Sahara entities, which were directed to refund money collected through Optionally Fully Convertible Debentures (OFCDs) to investors.

In 2015, SEBI ordered the winding up of Sahara Mutual Fund’s schemes due to non-compliance with regulatory requirements. The regulatory scrutiny and legal challenges indeed led to operational difficulties and affected investor confidence in the fund house.

Market segment

Despite being available in the market,[51] a recent report on Mutual Fund Investments in India published by research and analytics firm, Boston Analytics, suggests investors are holding back from putting their money into mutual funds due to their perceived high risk and a lack of information on how mutual funds work.[52] There are 46 Mutual Funds as of June 2013.[53] In 2019, Asset under management (AUM) of the mutual fund industry rose by 13% to 24 trillion in 2018 by November[54] The total assets under management (AUM) has surged by around 23.43% in 2023. The Assets base in January 2023 was Rs.40.70lakh crores, which rose to Rs.50.24 lakh crore in Nov, 23.

Average assets under management

Assets under management (AUM) is a financial term denoting the market value of all the funds being managed by a financial institution (a mutual fund, hedge fund, private equity firm, venture capital firm, or brokerage house) on behalf of its clients, investors, partners, depositors, etc. The average assets under management of all mutual funds in India for the quarter Dec 2015 to Mar 2016(in ₹ Lakh) is given below:

| Mutual Fund Name | Total Schemes | QAAUM AUM (₹ Lakh.) | Prev QAAUM (₹ Lakh.) | Inc/Dec (₹ Lakh.) | Percentage |

|---|---|---|---|---|---|

| Axis Asset Management Company | 263 | 3,776,454.37 | 3,456,348.88 | 320,105 | 9% |

| Baroda Pioneer Asset Management Company | 111 | 965,630.33 | 925,542.12 | 40,132 | 4% |

| Birla Sun Life Asset Management Company | 806 | 1,367,851.07 | 1,368,449.34 | 5,312 | 0% |

| BNP Paribas Asset Management Company | 114 | 509,706.79 | 500,795.21 | 9,209 | 2% |

| BOI AXA Asset Management Company | 76 | 238,501.41 | 242,767.91 | 2,887 | 1% |

| Canara Robeco Asset Management Company | 142 | 804,326.86 | 751,779.86 | 52,627 | 7% |

| Pramerica Investment Management | 142 | 804,326.86 | 751,779.86 | 52,627 | 7% |

| Canara Robeco Asset Management Company | 142 | 804,326.86 | 751,779.86 | 52,627 | 7% |

| Canara Robeco Asset Management Company | 142 | 804,326.86 | 751,779.86 | 52,627 | 7% |

| Canara Robeco Asset Management Company | 142 | 804,326.86 | 751,779.86 | 52,627 | 7% |

| Canara Robeco Asset Management Company | 142 | 804,326.86 | 751,779.86 | 52,627 | 7% |

| Canara Robeco Asset Management Company | 142 | 804,326.86 | 751,779.86 | 52,627 | 7% |

| Canara Robeco Asset Management Company | 142 | 804,326.86 | 751,779.86 | 52,627 | 7% |

| UTI Asset Management Companyy | 1220 | 10630921.82 | 10630921.82 | 52,627 | 0% | Gross | 11856 | 135912187.2 | 132170477.1 |

Mutual Fund Acquisitions

| Seller | Acquired By | Year |

|---|---|---|

| Pioneer ITI MF | Franklin Templeton | 2002 |

| Zurich India AMC | HDFC MF | 2003 |

| Alliance Capital MF | Birla Sunlife | 2005 |

| Standard Chartered | IDFC | 2008 |

| AIG Global Investment Group MF | PineBridge MF | 2011 |

| Benchmark Mutual Fund | Goldman Sachs | 2011 |

| Fidelity | L&T Finance | 2012 |

| Morgan Stanley's MF | HDFC MF | 2013 |

| PineBridge MF | Kotak MF | 2014 |

| ING Mutual Fund | Birla Sunlife | 2014 |

| Daiwa AMC | SBI MF | 2013 |

| Goldman Sachs | Reliance MF | 2015 |

| Deutsche | Pramerica | 2015 |

| JP Morgan | Edelweiss | 2016 |

| Peerless | Essel | 2017 |

| Escorts | Quant | 2018 |

See also

- Risk management

- Financial risk management

- 2020 stock market crash

- Satyam scandal

- Great Recession

- 2008 financial crisis

- Dot-com bubble

- 1992 Indian stock market scam

- 401(k)

- Roth IRA

- Bombay Stock Exchange

- National Stock Exchange of India

References

- MF History". Association of Mutual Funds of India.

- "Indian Mutual Fund Industry's Average Assets Under Management (AAUM) stood at ₹ 57.01 Lakh Crore (INR 57.01 Trillion)"

- "SEBI | Annual Report 2021-22".

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.

- Agarwal, Nikhil (24 May 2023). "50% mutual funds get redeemed within a year. Is long-term investing dead?" The Economic Times.